The End of NIRP

Welcome to my Substack

These are long form notes im using to formalise my investment framework and explore the world of content creation. If what I have to say is interesting to you or your peers, please hit the subscribe or share. The content will always be free and I welcome criticism and discussion.

On a final note - these notes are written anonymously but in the case you decipher my identity, they represent my personal views and not those of my employer.

Let’s get into it.

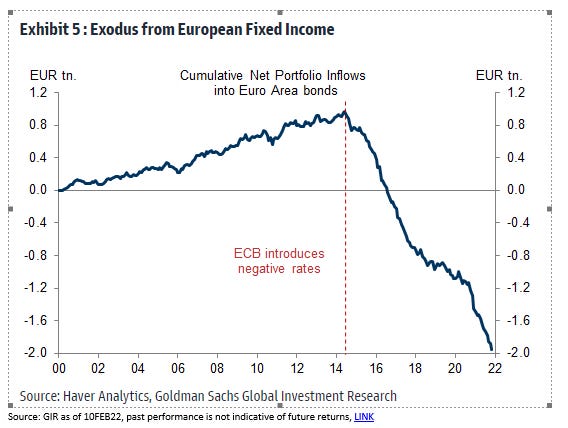

Negative Interest Rate Policy is being priced to end globally.

This has been a spectacular driver for flows – as can be seen from European Fixed Income Flows below from GS

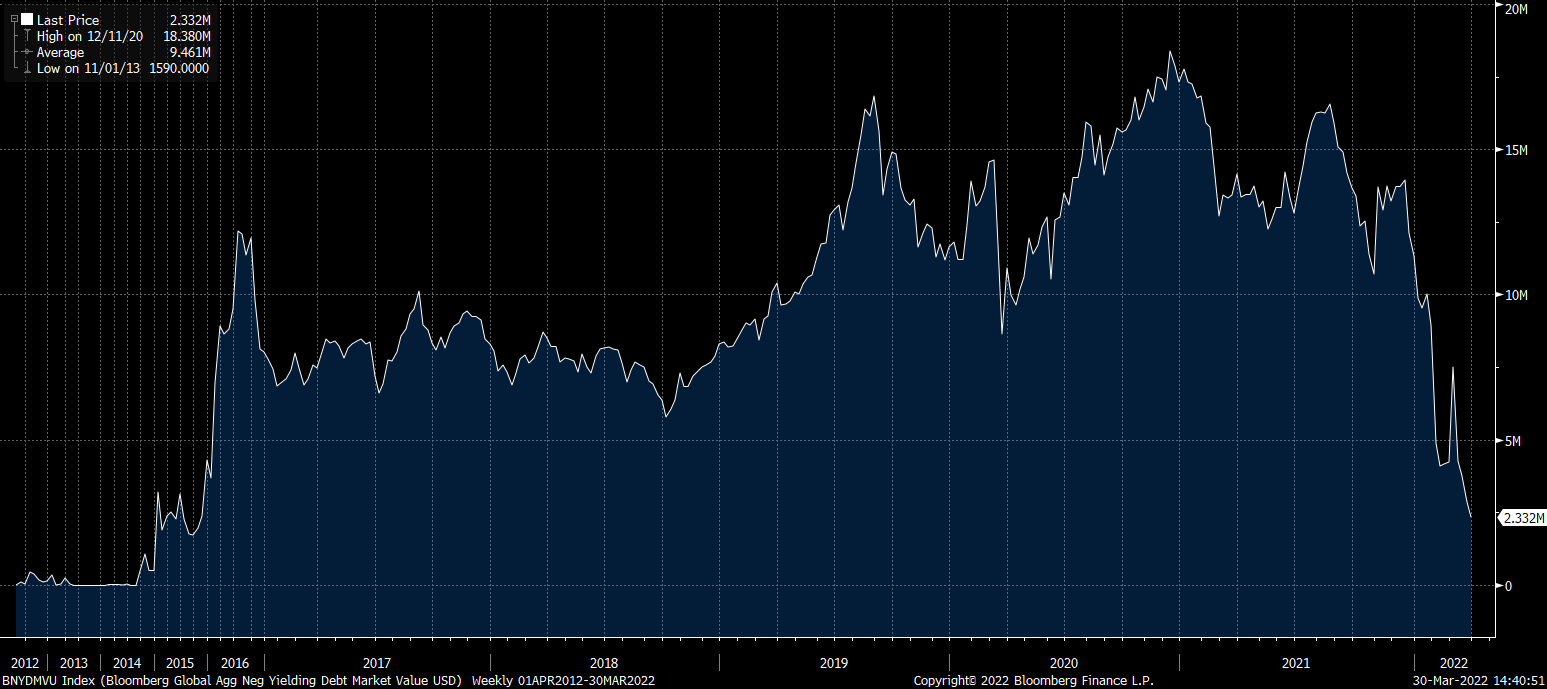

The total stock of negative yielding debt has fallen from ~18tn USD to 2.3tn USD - the bulk of which are very short term bonds/bills

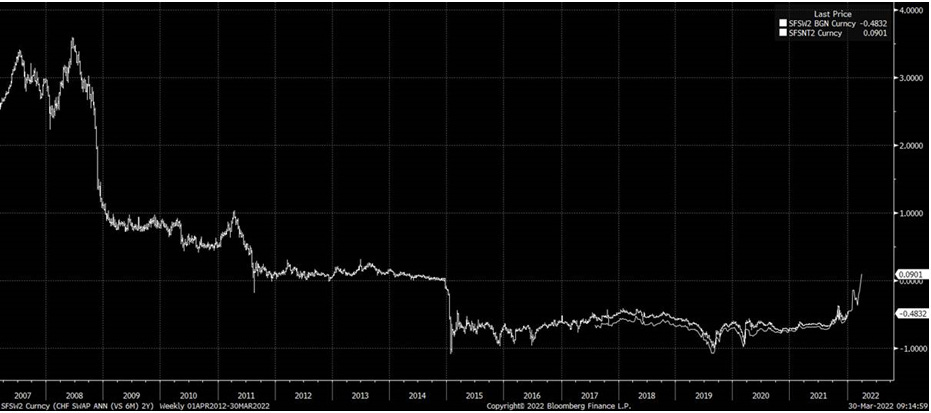

2y rates are now positive globally for the first time in 8 years

Switzerland

Germany

Japan

If you look at when these policies were implemented – it really accelerated the outperformance of US assets. Below is a chart of Wilshire 5000 (all US stocks) vs. Stoxx 600 (most EU stocks) in USD

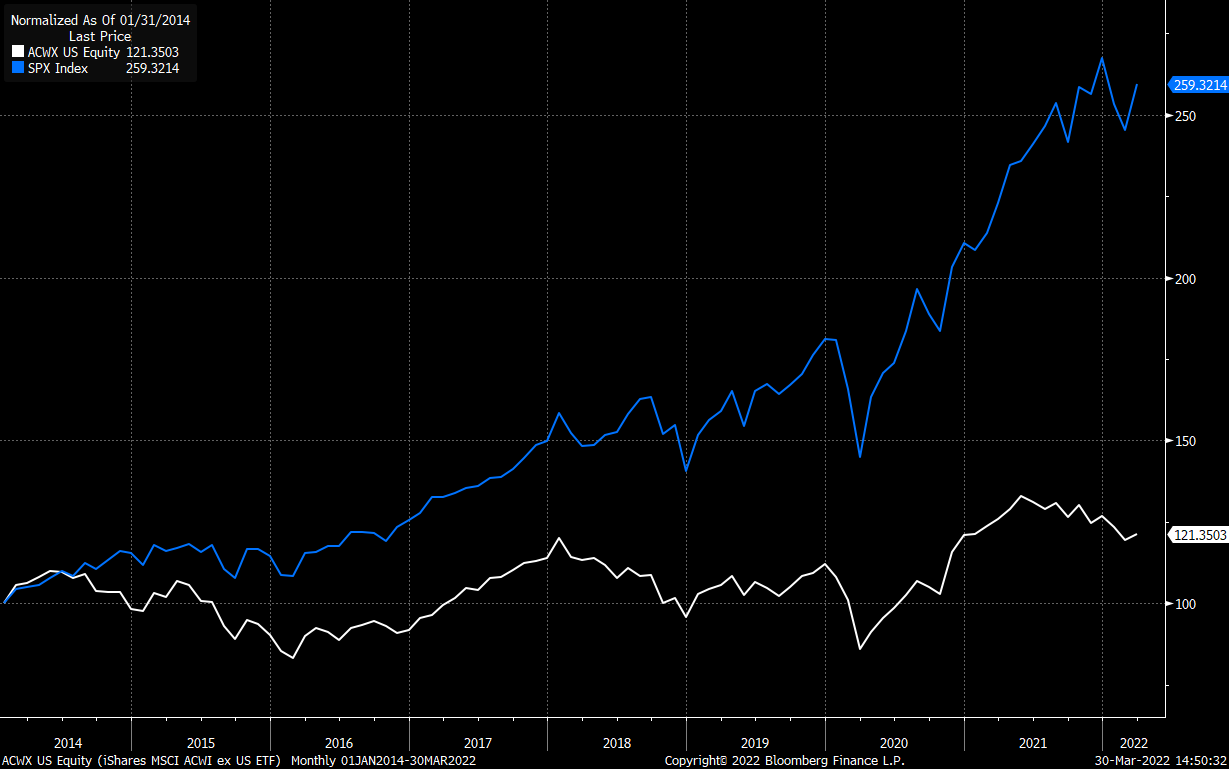

Another way to look at this is the performance of SPX (Blue Line) vs. MSCI All Country World Index ex US (White) line since 2014 when the policies were introduced.

We can see how pronounced these flows were by looking at the global liquidity flows in the US (black line)

However these flows are starting to reverse - as can be seen with the blue line for Europe above - which is leading to capital flows that are more favorable to ex US.

Without these flows - and with a potential reversal of flows from the last decade - the US is more likely to be judged on its domestic economic situation. This is likely to highlight its unfavorable dual deficit.

There is an enormous amount of recency bias around US exceptionalism - however the world is changing fast. In finance you are paid to adapt and, to me, it looks like the facts are changing.

Good Luck