The Deluge is Close...

At the start of the year - I shared my thoughts on why I expected both CNH and Commodities to weaken.

There was a period of divergence where I questioned if we were entering a new regime or a VAR event was close.

My leads all faced deeply negative for commodities.

As Asia has weakened - we have seen one leg of the growth stool aggressively kicked away. This left Commodities trading with a Ukraine War Premium against a rapidly faltering European Growth and the US continuing to outperform everyone.

The market was very focused on supply stories across the commodity complex.

Asian FX vs. Commodities

We are now starting to see the first signs that US demand is faltering quite materially

For Instance - Gasoline Demand is slowing aggressively

This leaves us with a scenario of Weak Asia, Europe and US.

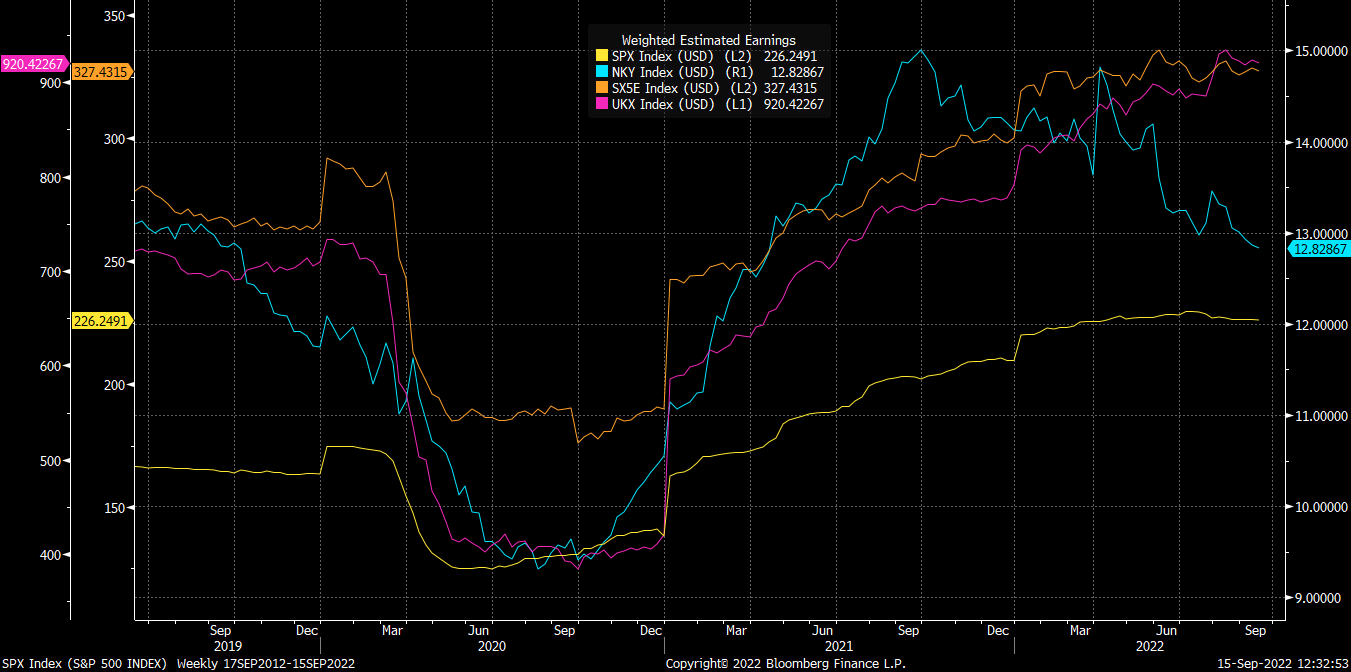

Yet when you look at Earnings Estimates for Global Equity Indices in USD they are all trending up except Japan due to currency devaluation

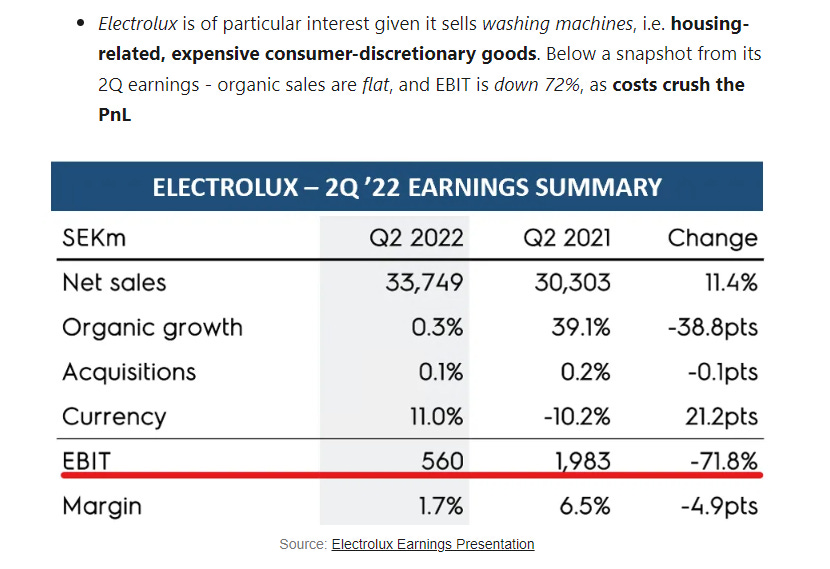

The excellent Substack from Florian Kronawitter (nexteconomy.substack.com) revealed just how far this is from reality with an example from Europe

At the same time this is happening - Central Banks are aggressively hiking when raw asset prices are suggesting they should have stopped

Lets look at how metals price vs. rates.

A good metric for the front end is the Copper vs. Silver ratio

Here is the Long Term Chart vs. US 2y2y

If we look at the more recent period - you can see that we peaked nearly 1y ago

If we look at the middle of the Treasury Curve - The best lead has been Copper vs. Gold.

You are able to see that the growth expectations embedded into Metals have materially diverged from the rates this year.

And finally the long end has been more anchored to the Silver vs. Gold Ratio. This correlation is looser but performance of silver over gold have tended to kickstart inflationary surges by about 1q and bonds tend to overshoot before resuming to trend.

What I have observed is that Silver/Gold tends to follow UST Term Premium.

And what you tend to see is that Term Premia is a relatively good metric for the trajectory of EPS growth.

So our assertion is that Earnings are going to be A LOT lower than the market is ready for and the FED by ignoring growth concerns is causing more damage under the surface

Firms are now getting hit from all angles.

Slowing Demand

Surging Costs - mainly stemming from Energy and Labour

Expensive Rollover costs for debt financing

This is where it gets tricky - without downside trajectory in Core Inflation, if Central Banks choose to stimulate - they can improve the scenario of 1 & 3 but at the expense of more issues in 2. Moreover - the market has inflation on the brain - stimulate aggressively and 3 will move against you shortly afterwards.

For this reason - they essentially have to wait for the market mechanism to destroy enough demand to facilitate a pivot.

This is going to be an ugly period and it isn’t going to be quick recovery - imbalances must be resolved

How far should EPS fall..

Michael Belkin who I highly respect has a 2023 EPS target on the SPX of 107.

The Term Premia analogue sees -25% Earnings off of 204 Trailing - so ~150

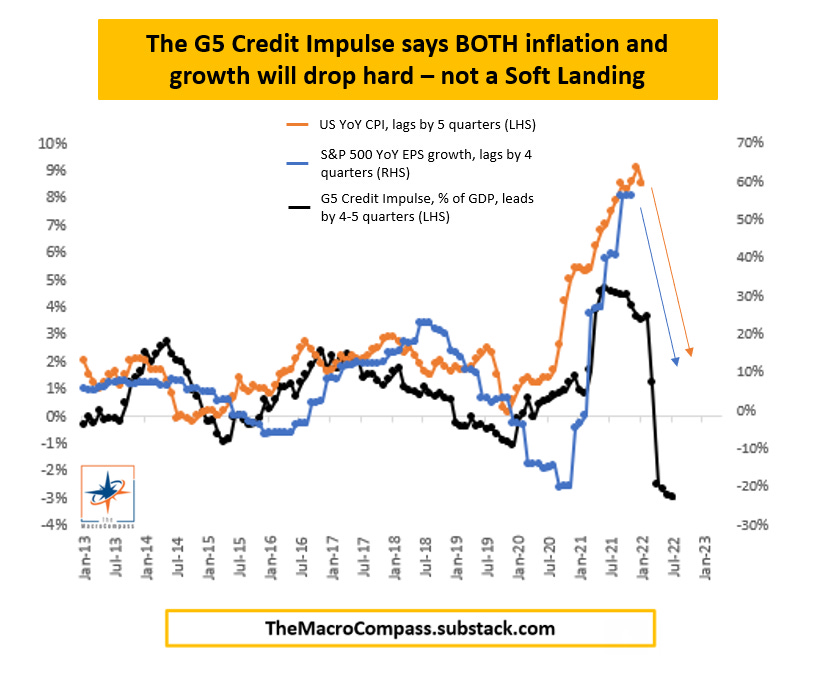

The G5 Credit Indicator see a similar -25% EPS Growth

This is vs. a street estimate of 226

With rates unable to move until the FED truly pivots - this is going to leave the market with only one option and that is to sell Equity.

To illustrate how prevalent the rates discount factor has been over the last 25 Years - see the below chart.

Recreated from Alex Gurevich’s book - it shows 10y bonds 2y fwd as a lead to Equity

This indicator currently prices no signs of a bottom until the end of next year.

What are the counterfactuals?

In my mind - there are three material areas that could mitigate the scenario being outlined above

China stablises once Xi has cemented power next month - this would improve demand but provide support to inflationary pressures.

Governments fiscally make up for loss in market demand - again, this would improve demand but provide support to inflationary pressures.

Gov fiscal is tricky - spending is largely targeted at Green Initiatives within the economy. The leakage of this into the wider economy is harder to determine

Equity exposures are low on a recent lookback - this is a kind of fickle point, for every seller must be a buyer in the cash equity space. Equities in 08 fell 40% despite the market being underweight and bearish.

What to do?

I still find bonds interesting - without them rallying, Equity is only going lower. This makes them the lesser bad evil to me.

Gold is also getting interesting - wait for strength

In my mind …the deluge is coming