Honey I'm Home - Thoughts on Housing

Honey I'm Home - Thoughts on Housing

Finance/Trading is Hard.

Getting the aggregate cyclical direction is a challenge but achievable for those prepared to do the work. However - timing is hard.

Timing being hard is why risk management is so important.

Can you stay in the game long enough that when your view is confirmed, you are able to monetise it. This is essentially the game.

I have got some things very right and some things very wrong this year.

Let’s start with the latter

I thought the combo of European Fiscal + Hawkish ECB would drive flows into Europe (or prevent outflows) which would be good for both the currency and the PIGS. Whilst the PIGS are actually trading relatively well all things considered - the EUR has taken it on the chin from the combo of tight USD liquidity and a huge terms of trade shock emanating from the Ukraine conflict.

This is equal weighted PIGS - I still like the trade. YTD PIGS is -9% vs. SX5E -21.5%

However the USD leg has been a nightmare. In hindsight - I’m an idiot. I have been pitching tighter credit, lower commodities and a flatter curve - none of which scream weak USD. I even wrote that I expected CNH to depreciate vs. USD in a substack article. We live and learn.

So what have I got right - well I generally expected some turbulence.

We are likely to see a reasonable mean reversion between US and Chinese inflation over the next 1-2y. In doing so - this will create a material amount of depreciation pressure on CNH given the extremes to where its trading vs historic funding differentials.

Any mean reversion is likely to set off elements of reflexivity. In general – a strengthening CNY is associated with higher commodity prices and vice versa.

And if correlations were to hold - commodities were in trouble

From a portfolio perspective – we can raise the following hypothesis’

1. Either USD or Commodities are materially mispriced and there is a significant VAR event in the making

2. We are entering a completely new regime than the last 40 years which will require vastly different portfolio theory.

And that macro volatility was likely to pick up a lot as policy seemed to be pissing into the wind.

So we find ourselves in this very odd situation where you have an inflationary fire burning, on one side are the FED acting as the Fire Brigade pouring water on the flames and on the other you have Xi & Biden adding gasoline. This is likely to be a very challenging environment across the board.

If the policies of Washington and Beijing continue to stimulate - the FED is going to be forced to go bigger than people are ready for to prevent entrenched price rises. IF they do so - those with high leverage are going to have to be sacrificed.

Things are about to get very volatile.

However - as alluded to in the intro - timing is everything. We can use the leads to understand the pre-conditions but knowing when to press the accelerator is tricky. This is a FANTASTIC environment for CTAs who are happy to play ‘price goes up - buy’, ‘price goes down - sell’.

I am always on the hunt to try and improve my timing/leads. Stanley Druckenmiller recently gave an interview for Ira Sohn with Patrick Collison

In the interview - Stan tells us that what he does is group companies into leading economic indicators and then listens to what management says. I have never really taken this approach before - I have usually used the relative prices to discount where the market is likely to go.

So this week - I have been on a deep dive into earnings calls for leading parts of the economic cycle like housing.

I have been pretty surprised at what i’ve heard.

I went into the calls expecting to hear about emergent weakness in the housing sector.

Rates up, Liquidity Down, Slowing Job Market, Real Incomes Down

I think most people in macro finance are using the same logic.

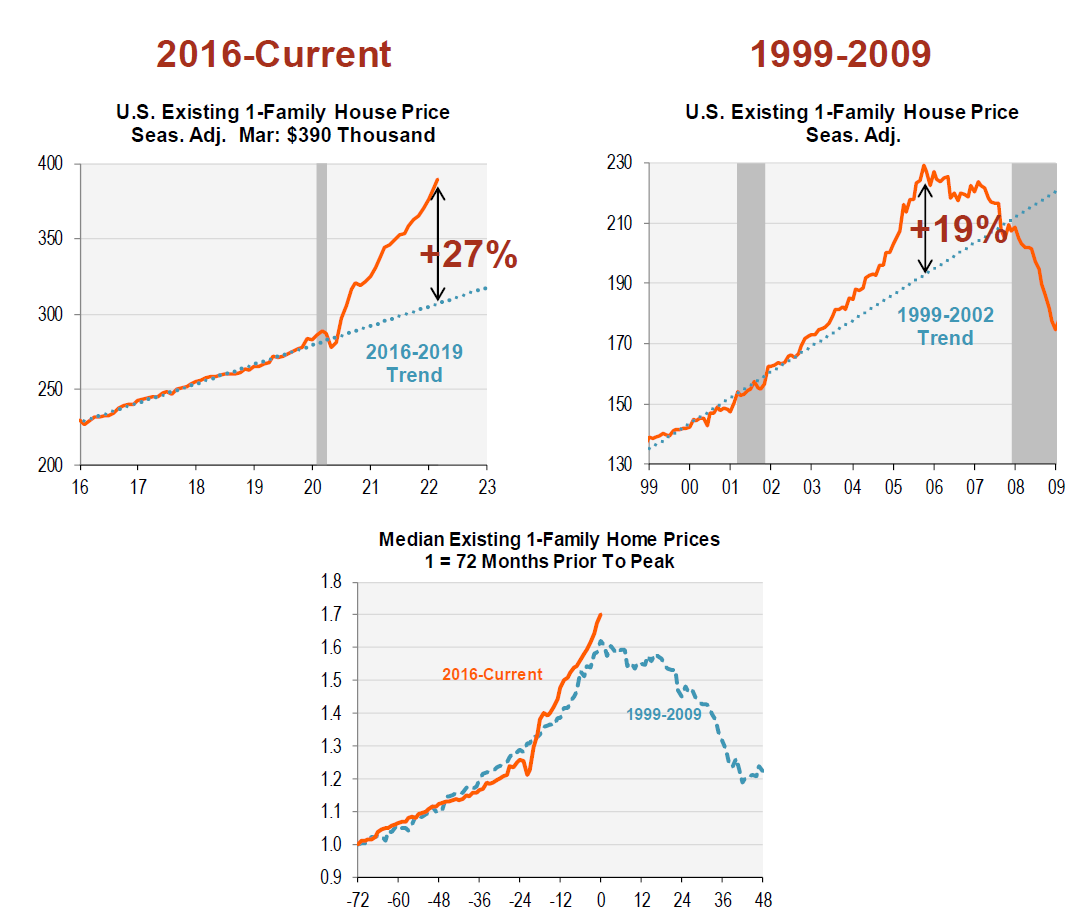

Housing is egregiously overvalued vs. trend

Pretty decent lay up for a significant fall I was thinking.

However - today is not 2006

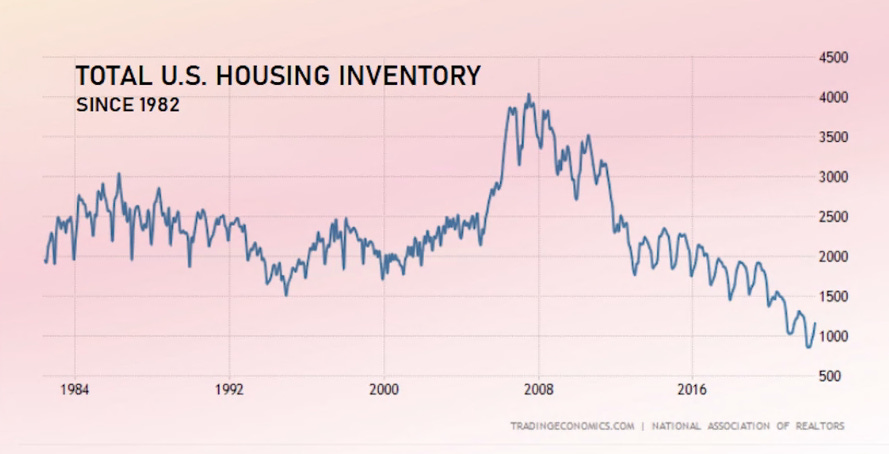

Firstly - there are not many houses

A scenario that the pandemic made far worse.

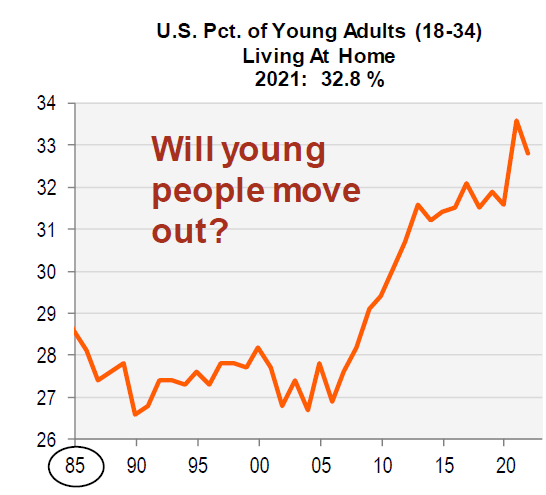

Secondly - there are an entire demographic (mainly Millenials) that have not moved out of home for a variety of reasons

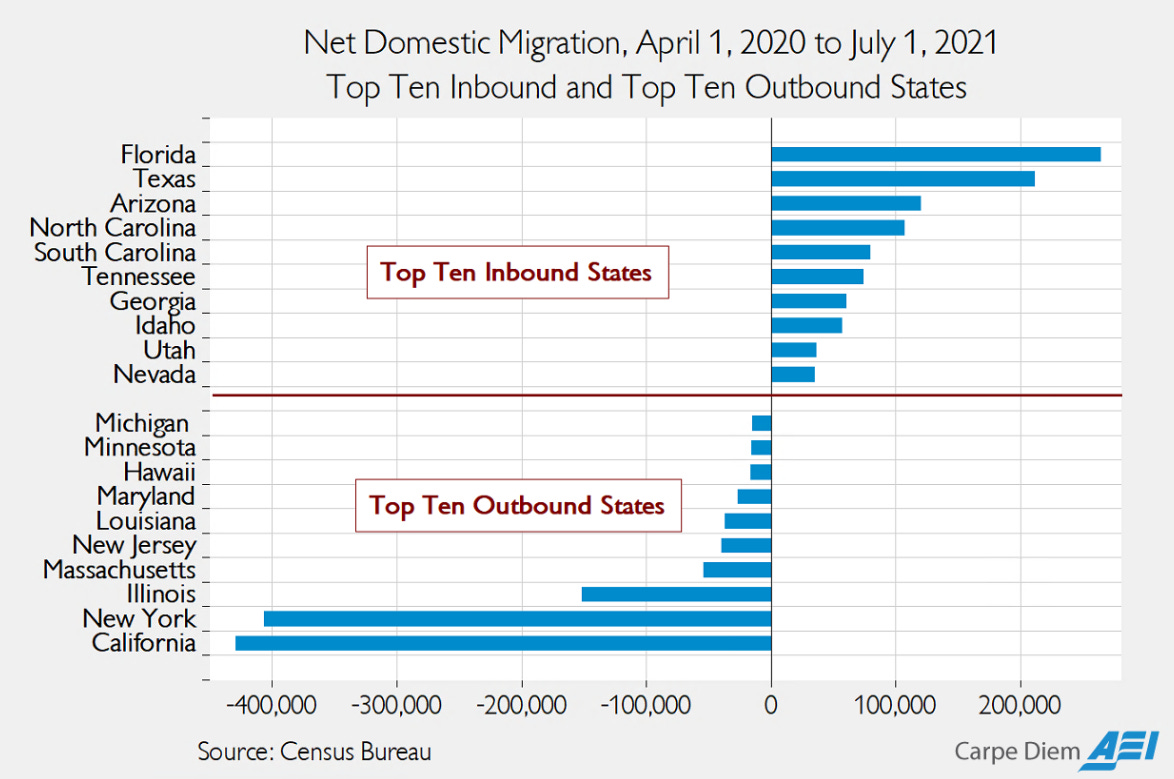

Thirdly - geolocation means less in an era of remote working. Young workers are able to migrate to cheaper areas and lay down their roots.

Now I hear many very smart peers say that Macro leads Micro which may well turn out to be true but I thought this quote from the DR Horton Q2 Earnings call was pretty revealing.

The rate increase is eliminating some people from the home buying experience but we still have more people try, qualified buyers trying to buy homes, and we can produce today. One of the things that really I think has impressed me back in 2018 when you saw a rapid rise in rates demand just was significant level reduced. And then after rate shock was kind of mitigated, we saw demand come back and come back strong. But through this cycle, which is in even a more rapid rate increases, yes, we've had people that don't qualify anymore, but the demand side is still very strong. The desire to own homes and it may be the fact that prices have escalated very fast and rents are escalating even faster than the price of new homes and all the talk about inflation and then locking in your housing cost for 20 years. I mean home ownership is a cherished thing today and the people coming out of the, the millennials coming out or even individuals relocating from other markets to kind of where the growth is taking place. They want to own a home, they want to lock in their housing cost and they want to get in the neighborhoods that they can raise families in.

The Toll Brothers earnings call echoed a similar sentiment.

We therefore have an large conflict starting to arise between the financial economy and real economy.

DR Horton vs. SPX

I notice that firms that are engrained within this trend are no longer following the correlation of Yields Higher/Housing Lower.

White Line = DR Horton/SPX

Blue Line = TLT (20+ Year Bond ETF)

When assets aren’t following historical correlations - it’s worth paying attention.

There are ~75m in the 18-34 demographic within the US - to mean revert to the average could be a demand of up to 3.75m homes just from those leaving their parental home. There simply are not enough houses to cater for this level of demand.

The macro impact of this as a phenomenon is not to be underestimated.

We are used to large deflationary pulses creating the backdrop for large eases of FED policy via lower rates and liquidity injections.

Two of the core tenets of these pulses are rapidly declining oil prices and housing stress.

Significant underinvestment in Oil and ongoing geopolitical issues are significantly capping the left tail in the energy market; and it feels that with Millenials on the bid in an inventory short housing market, the left tail in housing is not as big as the macro would have you believe.

Any ease by the FED with this as a backdrop is likely to very quickly ignite commensurate inflationary pressures in the system.

Good Luck