CNH Dilemma

Welcome to my Substack

These are long form notes im using to formalise my investment framework and explore the world of content creation. If what I have to say is interesting to you or your peers, please hit the subscribe or share. The content will always be free and I welcome criticism and discussion.

On a final note - these notes are written anonymously but in the case you decipher my identity, they represent my personal views and not those of my employer.

Let’s get into it.

Over the last week - I have been asking many of my peers about what I view as a pressure cooker building in CNH. Many, are rightfully, pre-occupied by other areas of macro and the ongoing Russia/Ukraine conflict. However - to me - CNH is pretty interesting and I want to share a few thoughts and charts below to show you why.

China has been running very tight policies vs. the developed world for nearly 18 months.

At the same time - there has been a power grab going on in technology - highlighted to the world by the cancellation of the ANT Financial IPO just days before the launch. The power grab common prosperity doctrine that has emerged in China has seen technology firms severely weakened - especially internationally.

Alibaba US ADR - Arrow marks the failed IPO

This preceded a larger sell off in Chinese assets as the cocktail of very tight policy and an unfriendly central authority have impaired the demand for Chinese assets.

Golden Dragon China Index

Added to the technology selling has been a severe crackdown on the property sector - and the rampant speculation that occurs within it - by the CCP. There is a great follow on twitter below that has been providing timely updates to the onshore scenario below:

However - at the same time - CNH has become the strongest major currency in the world since both 2020 and 2021 to now.

So what’s going on?

My view is that China has been running very tight policy to crush any inflationary pressures.

As the rest of the world has gone on a rampant money binge - the CCP - who are able to take a more long term view - have seen the wood for the trees early and slammed on the breaks. Nothing would be more destablising to the power of the CCP than widespread inflationary pressure.

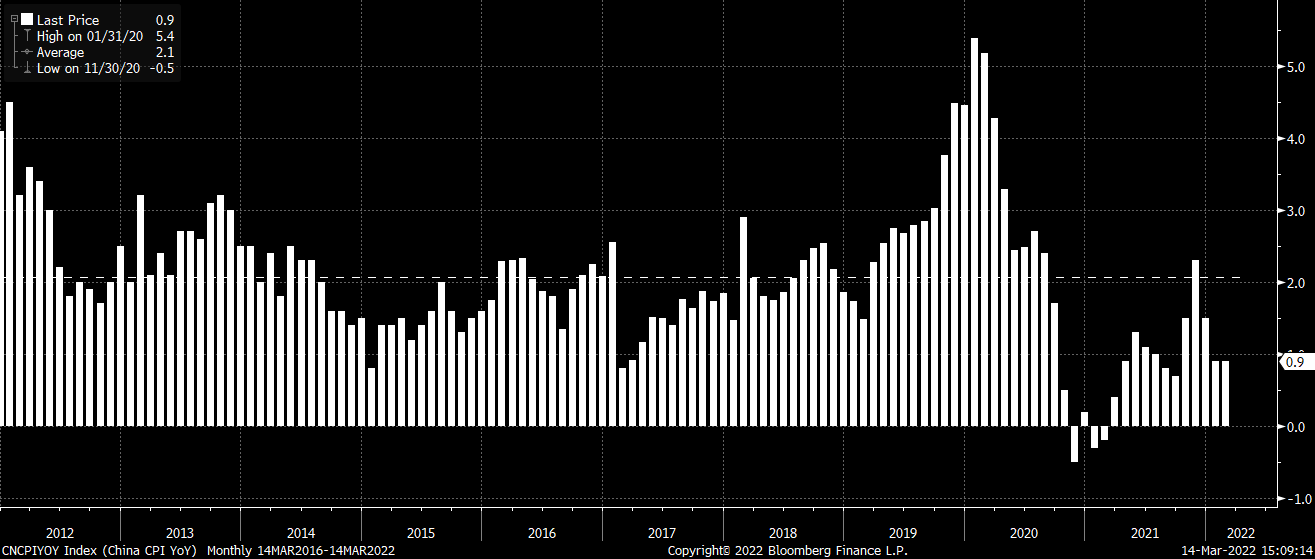

Chinese inflation is trading well below its 10y average of ~2% as a consequence.

However - in doing so - this has pushed real interest rate differentials massively in favor of China leading to a far stronger currency.

This can be seen quite clearly in the divergences from nominal funding rates.

White line = 3m Libor vs. 3m Shibor

Blue Line = USDCNH (90day lag)

Chinese CPI - US CPI

We can see that the divergence between the nominal rate differential and currency rate can be explained by including inflation to create the real rate differential

We can therefore see that the relative inflation rates between China and the RoW are going to have a major impact on the level of CNY currently.

Should we expect mean reversion?

I expect so.

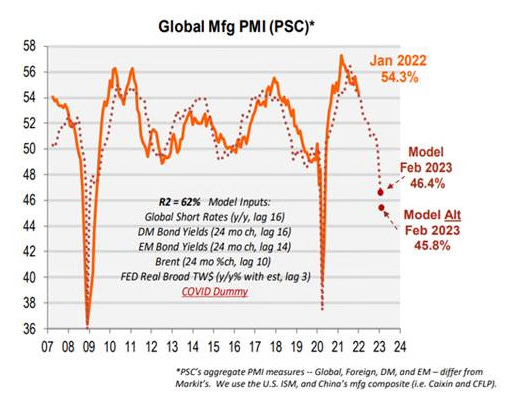

Looking at where the Global PMI leads are currently pointing - the rate of change in global growth is going to turn lower.

The US rates market has been picking this up for the last 6 months as 5s30s OIS has aggressively flattened.

The Macro Compass G5 indicator also suggests similar.

Moveover - given that inflation is a Rate of Change measure - over the medium term it will experience negative cyclicality.

Ok so the above covers why developed world inflation is likely to moderate over the medium term - what about China?

China is currently embarking on every disinflationary policy it can, namely:

Crushing domestic financial assets

Taking all the steam out of the property markets

Locking down the domestic population for omicron (which we know from the West to be unnecessary)

The first two items have already started to show cracks in the Chinese economy and given recent targeted easing in the short-term loan markets - have likely reached their limit without imposing material downside risks.

As for number 3, lockdowns are a temporary policy lever (we hope). Now there is a counterfactual here - one could argue that lockdowns in industrial China will further supply chain issues in the Western world which will create further stickiness in the inflation data. It is a fair point - the major difference to 2020 being that we are now in a contractionary liquidity environment, which will taper demand.

However - the aggregate point is that the disinflationary levers that Beijing can pull are quite limited now. If anything, they have already pushed too hard and parts of the economy desperately require material easing.

I would therefore hypothesise that we are likely to see a reasonable mean reversion between US and Chinese inflation over the next 1-2y. In doing so - this will create a material amount of depreciation pressure on CNH given the extremes to where its trading vs historic funding differentials.

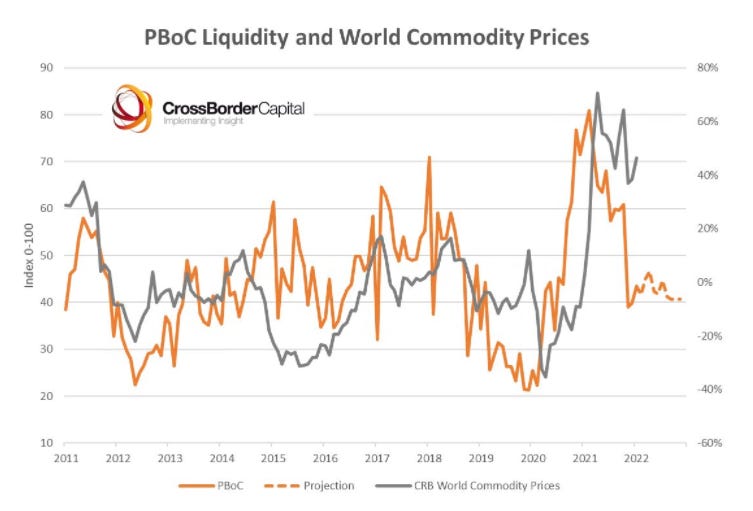

Any mean reversion is likely to set off elements of reflexivity. In general – a strengthening CNY is associated with higher commodity prices and vice versa.

CNYUSD (Blue Line) vs. Raw Commodities (White Line)

It appears to me that upcoming policy decisions – especially on the Chinese side – are likely to have relatively profound investment implications based on historical correlations.

Good Luck

This is very interesting and clearly written - thank you. Quick question: the Global PMI figure - is that from Nancy Lazar?

Great write up. I largely agree with the US/China inflation mean reversion thesis over 1 - 2y, but going forward I am deliberating the net effect of the demand-destruction potentially brought about by hawkish MP in the west vs gradual easing from PBOC. If it is clear that western governments can no longer tolerate cyclicality in the business cycle, then I would have increased conviction that the disinflationary trend of the past decade may be over