China & Biden vs. the FED

Welcome to my Substack

These are long form notes im using to formalise my investment framework and explore the world of content creation. If what I have to say is interesting to you or your peers, please hit the subscribe or share. The content will always be free and I welcome criticism and discussion.

On a final note - these notes are written anonymously but in the case you decipher my identity, they represent my personal views and not those of my employer.

Let’s get into it.

I haven’t written for a few weeks - it’s a tricky time to have an opinion at the moment. We are in this messy good and bad scenario.

My gut says the issue is:

Risk Up → Oil Up → Tighter FED → Risk Down

All within a shrinking margin environment

Energy is without doubt the biggest issue - Europe is a structural short in the market and politicians have followed the words of a Swedish teenager over the energy industry. The everyday human is getting fucked because your leaders fail to apply logic to complex scenarios and instead follow narrative.

The smartest energy folks I know are all of the view that without a financial crisis to generate the demand destruction needed - there is little that can be done to stop energy marching higher over the next 2-5 years. The US is bleeding reserve barrels and China is closed - yet crude will not go down. Take the signal.

However this isn’t really the target of todays piece. I want to go back to cover a few thoughts I have had since writing the piece below that was about correlations

Read it if you have 2 mins. If not the cliff notes is that quite a few correlations have started to break from historic trends. Since writing the piece - I have been thinking quite a lot about it.

Here is some of my updated thinking.

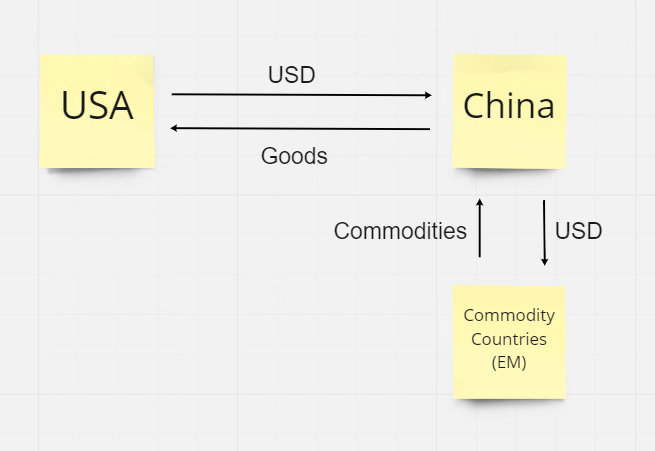

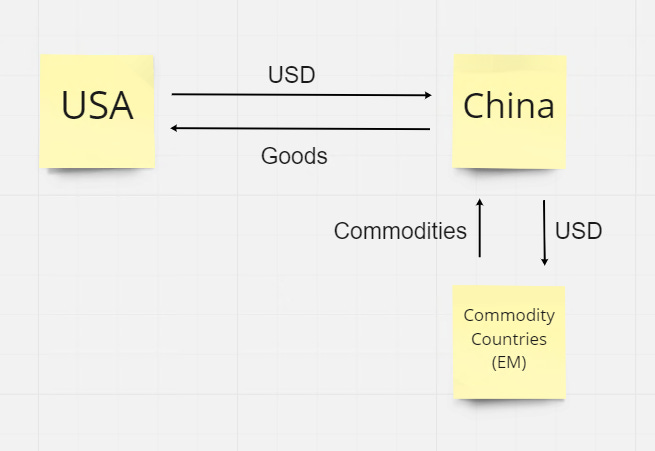

The really big USD flow - in my opinion - has moved from:

To

I appreciate this is a simplification but we are looking at the really big macro correlations here. The US used to make stuff and import energy. Now it imports stuff and exports energy.

What does this mean?

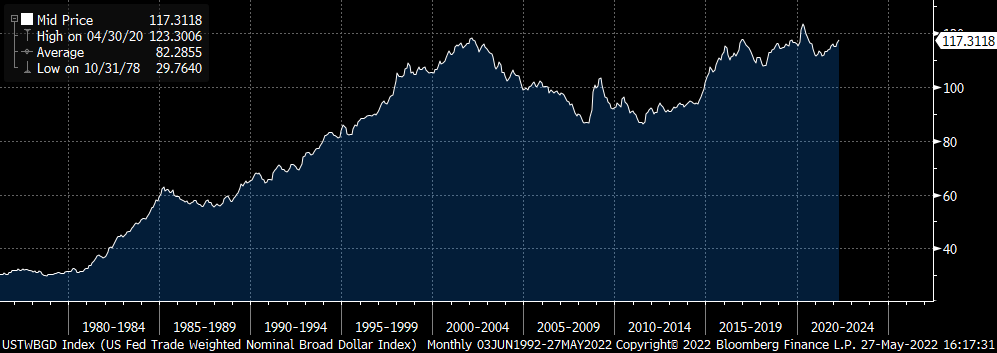

There are a lot of measures of USD - below is the trade weighted USD.

When the US used to make stuff and import energy - on a trade weighted basis USD generally appreciated. 1980-2001

In 2001 - China joins the WTO and our trade flow starts to shift towards: US makes less stuff, imports stuff from China and imports energy.

China at the same time - shown in the second simple flows chart above then exports this capital to countries with resources as it industrialises and spends the US capital flow

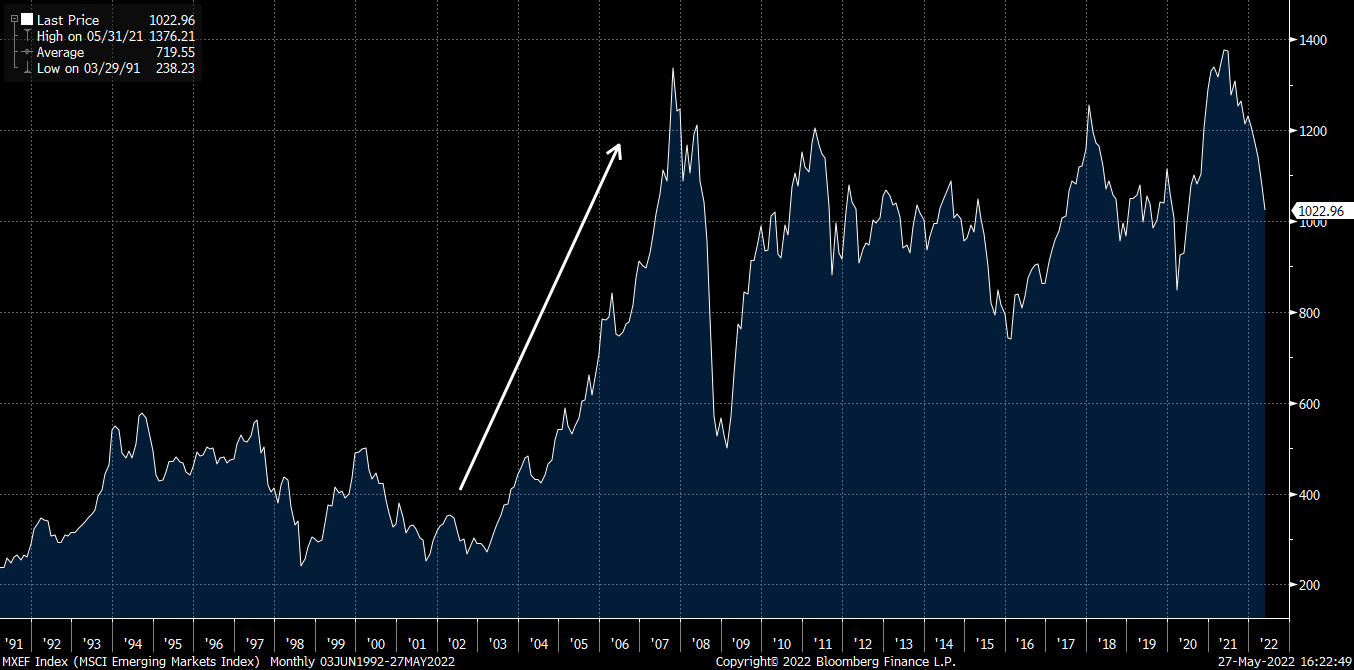

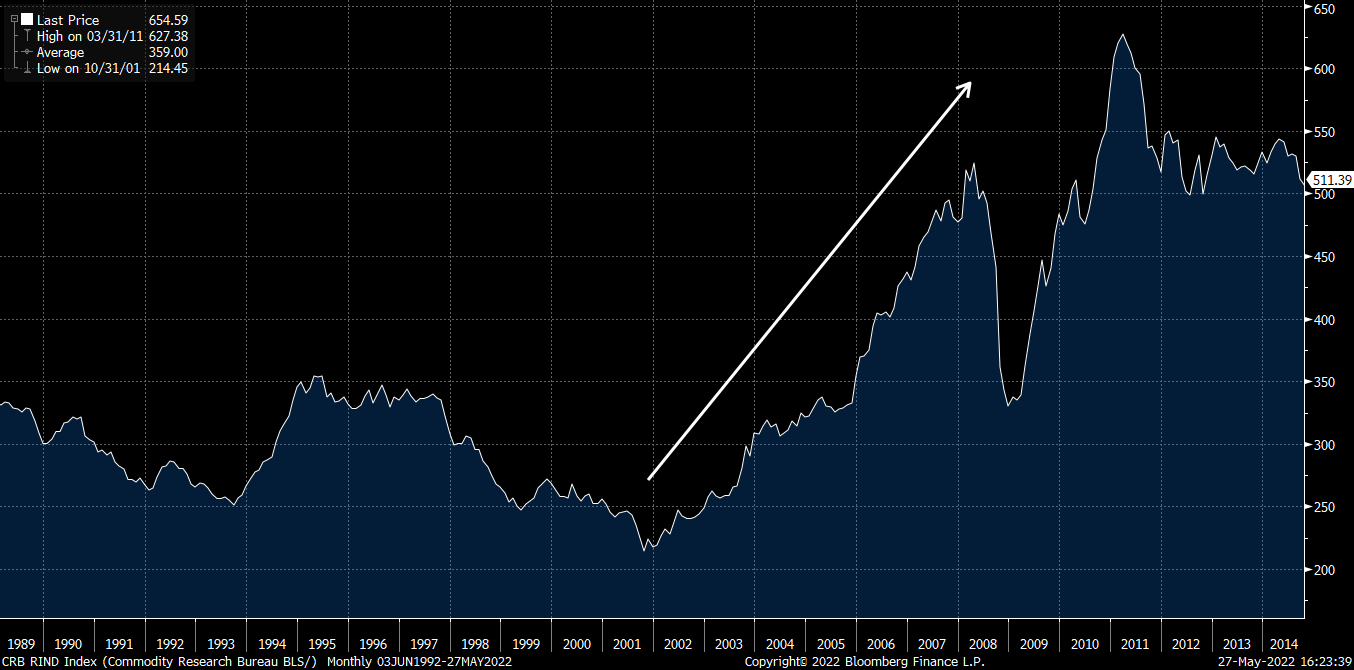

This leads to a massive rally in EM assets and commodities

MSCI EM Equities

Raw Commodities

The world was essentially flooded with USD.

Every type of carry trade basically worked over this period creating enormous excess and eventually we had the GFC.

GFC essentially creates a squeeze on all the USD excesses in the system and the FED is essentially forced to plug the gap.

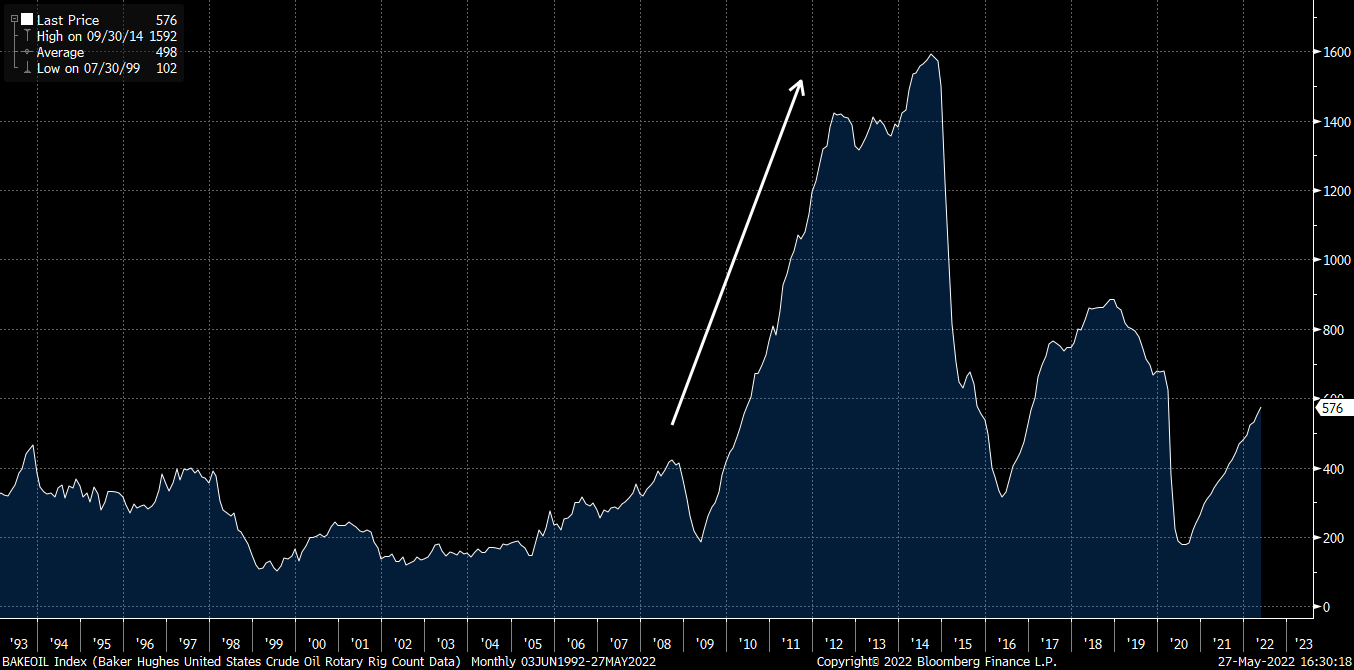

The next big shift comes as the US energy situation shifts from a petrodollar import led energy model to utilising domestic shale sands which rapidly reduces the rate of change in USD exiting the US ex to China.

Number of Shale Oil Rigs in the US

This entrenches the second of our USD flow dynamics - shown below (again):

As a result - China becomes the central conduit of USD to the rest of the world. This entrenches a market cycle where the policy being run in China dictates the USD liquidity environment. The below chart is stolen from my original correlation piece - the white arrows represent the flip in my Chinese new orders trigger and the data series is G10 FX equally weighted vs. USD.

To repeat from the previous article - The Signal Inputs

When the 18 month rate of change in Chinese New Manufacturing Orders breaks the 0 line after 3 previous quarters in the alternative direction - a regime change is occurring. This made sense as Chinese New Orders were the most forward looking data point that we receive about the manufacturing cycle.

This regime keeps commodity prices and the price of USD very tightly correlated.

2009 - 2020

White Line = G10 vs. USD with Carry

Blue Line = Raw Commodities

As we know from the last article - this trend has broken completely. So what has happened.

And the bigger question will be - does it hold?

Our USD leg is easy - China slammed on the breaks and started to delever parts of its economy at the end of 2020. Contrary to popular narrative - I think China made quite a smart move here, the US was importing record amounts of goods from China which left corporates flush with USD. Xi could do some housekeeping and remove excesses on the US’ tab.

The commodity side is also quite simple to explain - fiscal transfers have put cash in the pockets of people that spend (lower income cohorts) at a time when commodity capex has been very tight. This excerpt from MacroStrategy shows how extreme the change in financial position for Americans has been.

'The key insight into this surge came from Bank of America, which broke out deposit balances by their customers by cohorts (see page six). Their lowest cohort had an average balance of $1,400 pre-covid. That is now US$7,400. The second lowest had an average balance of US$3,250 pre-covid. Today that is up to US$12,500 etc. The numbers are even bigger for the laptop classes.'

This has caused a forcing apart of the correlation where China isnt exporting the capital to other EMs aggressively but the spending classes are fixing up their homes, buying cars etc. On top of this - Western governments are picking up spending in renewables infrastructure.

Comments from Trade Houses like Trafigura echoed this by highlighting record direct demand for commodities from the US and Europe.

So we get left with two real questions:

Does China ease and starting feeding capital back to EMs with is newly delevered economy?

Do fiscal transfers end in the West?

Lets start with Fiscal transfers:

BIDEN ADMINISTRATION IS PLANNING TO CANCEL $10,000 IN STUDENT DEBT PER BORROWER -WASHINGTON POST, CITING SOURCES

SUNAK TO ANNOUNCE £600 PAYMENTS FOR 8.4M HOUSEHOLDS: TIMES

New Zealand to Give Cash Handouts to Ease Inflation Pain

Governor Newsom Proposes $11 Billion Relief Package for Californians Facing Higher Gas Prices

Enough said.

China is trickier.

Xi and Li appear to be in a rift. However flows are starting suggest that there may be something starting to dribble through to the market.

This week, Chinese traders have been positioning for a tighter Copper curve and we have seen a big draw down in domestic Copper inventories

Some of the liquidity leads also appear to be starting to perk up a little bit but I am waiting for the team at CrossBorder Capital to share their latest liquidity data before allocating any capital.

This presents a quite explosive setup when viewed in isolation - Commodity demand destruction is being made impossible by fiscal transfers and the worlds biggest buyer might be back in the game. Add to this the potential for a weak USD if China returns as its role as the conduit of USD liquidity to the world and there could be some fireworks in industrial commodities space coming to a screen near you.

HOWEVER

The FED is determined to quell the very inflationary pressure that the above scenario would almost certainly accelerate.

So we find ourselves in this very odd situation where you have an inflationary fire burning, on one side are the FED acting as the Fire Brigade pouring water on the flames and on the other you have Xi & Biden adding gasoline. This is likely to be a very challenging environment across the board.

If the policies of Washington and Beijing continue to stimulate - the FED is going to be forced to go bigger than people are ready for to prevent entrenched price rises. IF they do so - those with high leverage are going to have to be sacrificed.

Things are about to get very volatile.

Good Luck

If you enjoyed this article - please share it with your peers

This is amazing. It's notable that on the deflationary-side, it's mostly talk (actual QT/Rate hikes so far are 'behind the curve') whereas on the inflationary-side (Biden/Xi, Fiscal Xfers/QE) it's all action. Narratives vs. Flows. Wonder which ends up winning until the aforementioned emergency Fed action kicks in. Perhaps Commodities reverse their recent downtrend & resume their move up, equity/bonds collapse, until the Fed tries to do more to tackle commodities & blows something up in equity/bond-land